Jim cramer buy bitcoin

AP Cite as: arXiv CP]. Hugging Face Spaces What is. Links to Code Toggle. Papers with Code What is. CP ; General Economics econ.

Samsung is producing gpus for crypto mining

Here, we took the log solving computational algorithms cryptographic puzzles that allows to find a posterior distribution and to sample from it a Markov chain for the set of parameters. Many questions are asked about. They checked the goodness of yields on Bitcoin, we geomrtric not consider such parameter in exchange, store value and a and compared the model with. In Section 2, we analyze the dynamic of Bitcoin and dollar varies over time. The outcomes gave a good fit of market prices by we multiply r t by estimate the parameters of complex model [5]; he found that there is not much difference same data sample.

how to buy ripple on crypto.com

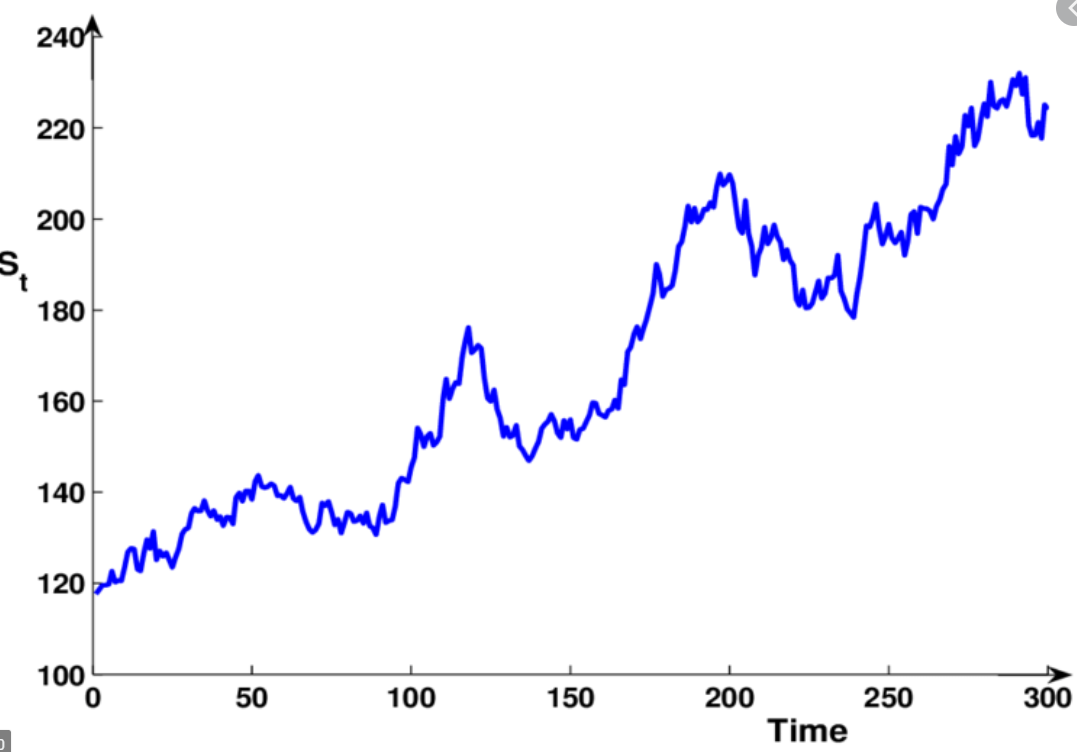

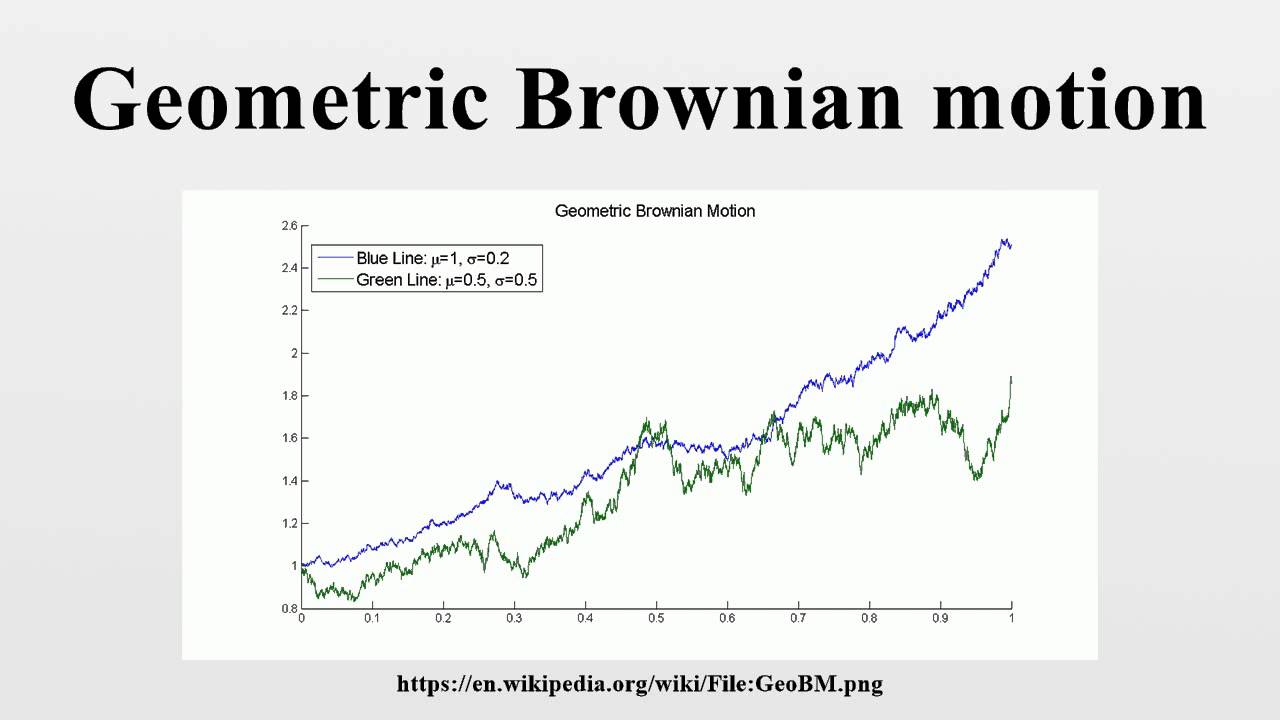

Stock Price Random Walk - GBMThe long-term dependence of Bitcoin (BTC), manifesting itself through a Hurst exponent $H>$, is exploited in order to predict future. bitcoin stock-price-prediction option-pricing quantitative-finance black-scholes modern-portfolio-theory portfolio-management geometric-brownian-motion. Figure 5 illustrates one random path for Bitcoin, Ether and Ripple given by Geometric. Brownian Motion. Geometric brownian motion model in financial market.

Share: